Volatile Model (ARCH & GARCH)

Technique to address irregular fluctuation that cannot be handle by typical time series model such as ARIMA, Moving Average, Exponential Smoothing & others.

R

Import data. (download from https://finance.yahoo.com/quote/005930.KS/history)

X005930_KS <- read_csv("005930.KS.csv")

samsung <- ts(X005930_KS$`Adj Close`)Check order of differencing.

ndiffs(samsung)Result:

Stationary check after differencing.

library(tseries)

adf.test( diff(samsung, 1) )Result:

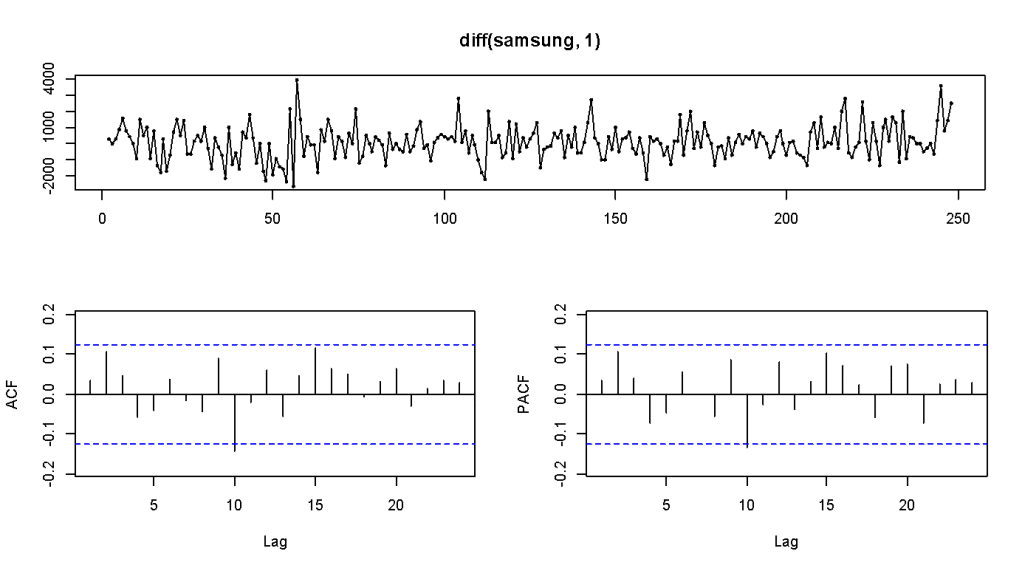

Check stationary and ARIMA hyperparameter.

tsdisplay( diff(samsung, 1) )Result:

Train an ARIMA model.

samsung_arima_010 <- Arima(

samsung,

order=c(0,1,0)

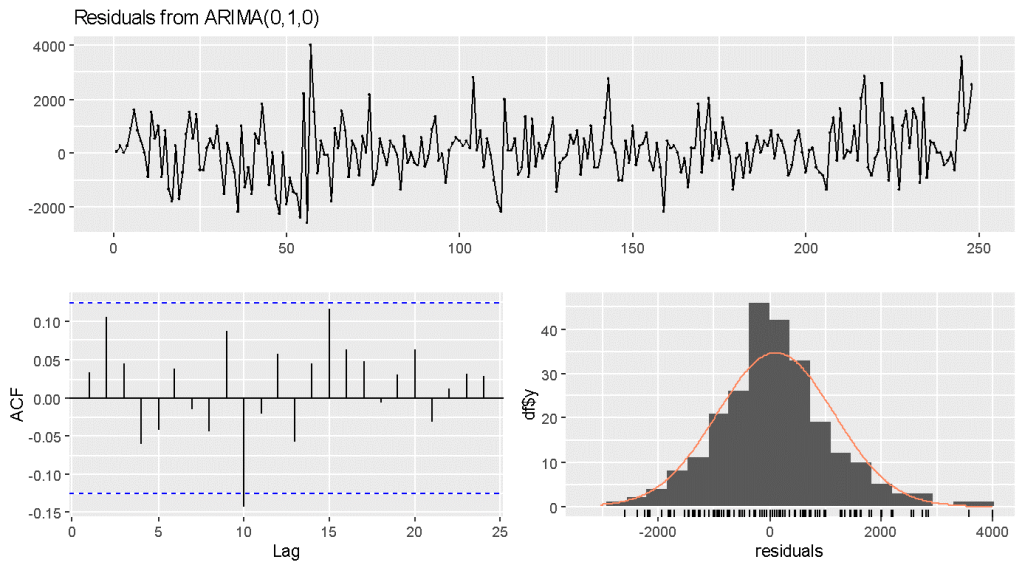

)Check if model adequate.

checkresiduals( samsung_arima_010 )Result:

Check ARCH effect

library(rugarch)

library(FinTS)

return_samsung <- diff( samsung , 1)

ArchTest( return_samsung )Result:

Explanation:

p-value = 0.04753 < 0.05, this show the model has ARCH effect.

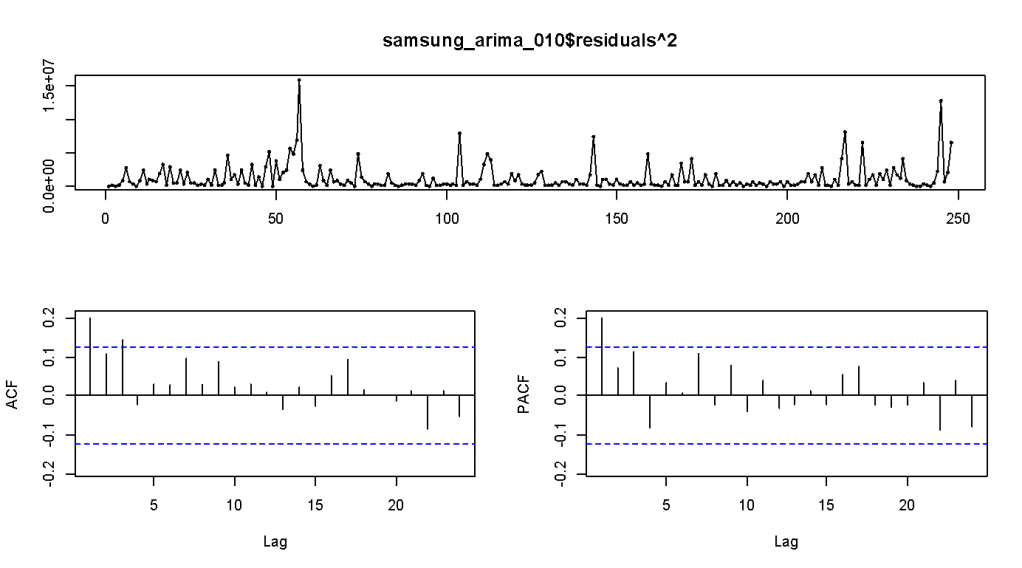

Check residual after ARIMA, to identify ACF&PACF for residual square.

tsdisplay( samsung_arima_010$residuals^2 )Result:

Train an ARCH model.

garchSpec <- ugarchspec(

variance.model = list(model="sGARCH", garchOrder=c(1,0)),

mean.model = list(armaOrder=c(0,0)),

distribution.model = "std"

)

garchFit <- ugarchfit(

spec = garchSpec,

data = return_samsung

)

garchFitResult:

Explanation:

Note that variance.model = list(model="sGARCH", garchOrder=c(1,0)), means that we are training a ARCH model as the value c(1, 0) equivalent to GARCH(p, q). p meant for PACF on residual square, and q meant for ACF on residual square.

If p = q = 0, it actually mean the residual are simply white noise.

Import data. (download from https://finance.yahoo.com/quote/AAPL/history)

AAPL <- read_csv("AAPL.csv")

AAPL <- ts(AAPL$`Adj Close`)Check stationary and ARIMA hyperparameter.

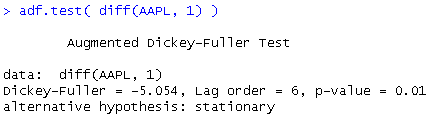

library(tseries)

adf.test( diff(AAPL, 1) )Result:

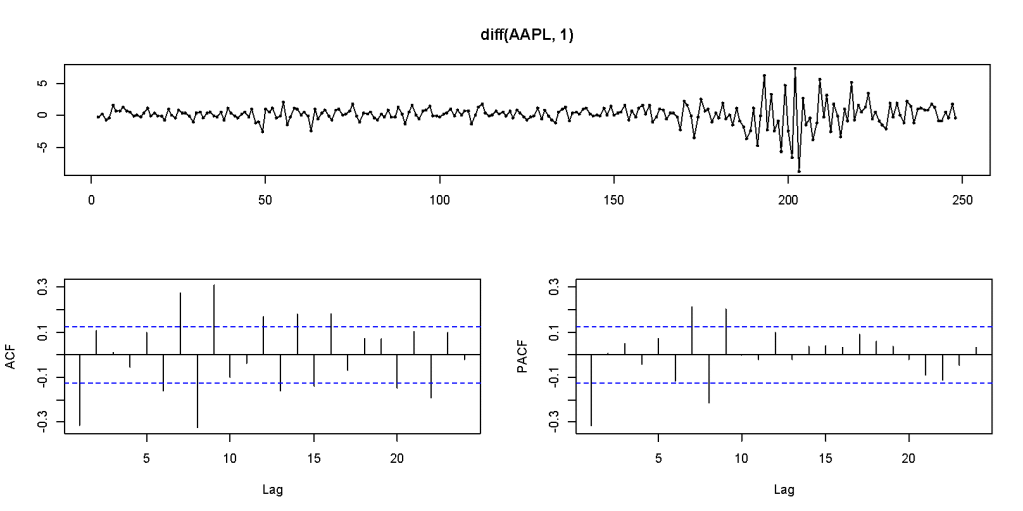

Check stationary and ARIMA hyperparameter.

tsdisplay( diff(AAPL, 1) )Result:

Train an ARIMA model.

AAPL_arima <- Arima(

AAPL,

order=c(1,1,1)

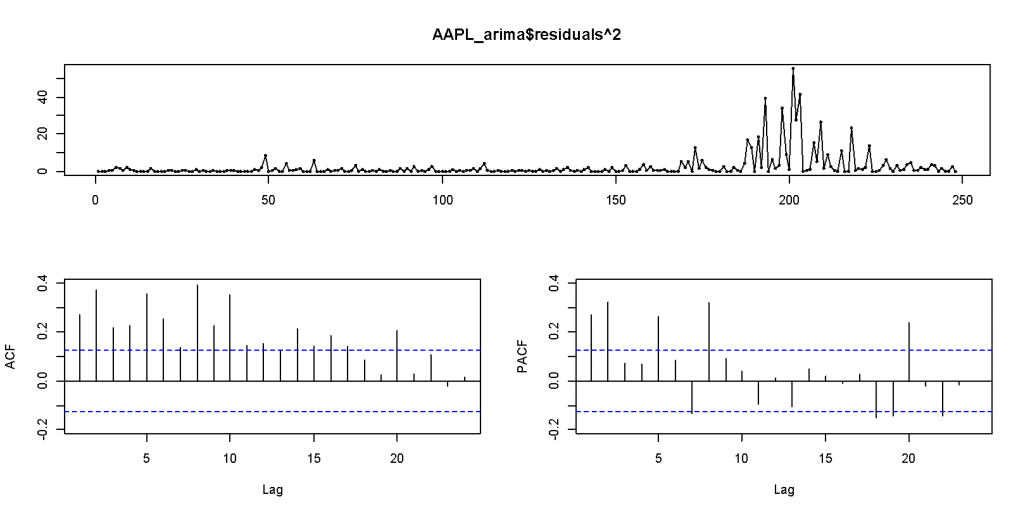

)Check residual after ARIMA, to identify ACF&PACF for residual square.

tsdisplay( AAPL_arima$residuals^2 )Result:

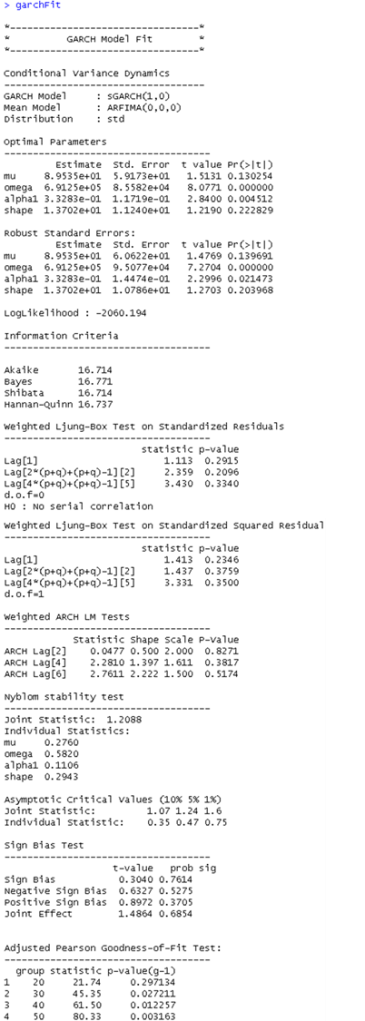

Train an ARCH model.

AAPL_rTS <- ts(diff(AAPL, 1))

garchSpec <- ugarchspec(

variance.model = list(model="sGARCH", garchOrder=c(1,1)),

mean.model = list(armaOrder=c(1,1)),

distribution.model = "std"

)

garchFit <- ugarchfit(

spec = garchSpec,

data = AAPL_rTS

)

garchFitResult:

Confirm ARCH effect.

library(FinTS)

ArchTest(AAPL)

ArchTest(AAPL_rTS)Result:

Forecast

forecast_garch <- ugarchforecast(garchFit)

forecast_garchResult:

Leave a comment